This industry still has a lot of upside.

I haven’t had cable or satellite TV in years. I only stream video content on demand from the internet these days. Millions of people are just like me, of course. And because adoption rates of streaming TV are so high, it’s easy to overlook just how fast this space is still growing.

Over-the-top (OTT) refers to streaming video regardless of what kind of device one uses to stream it. According to MarketsandMarkets, from 2022 through the end of 2027, global revenue for the OTT market is expected to more than double, an incredible expansion rate.

Connected TV (CTV) refers just to TVs that can connect to the internet. Research group eMarketer expects the U.S. CTV market to grow by 10% annually through 2027 and potentially even faster in international markets.

These aren’t necessarily authoritative studies on the subject, and forecasts are usually somewhat off. But other studies and analysts agree: Streaming video, particularly CTV, is still growing at an extraordinary rate, and growth is expected to continue for years to come. Believe it or not, Roku (ROKU -3.83%) owns almost half the space.

What’s going on with Roku?

In its letter to shareholders in the second quarter of 2024, Roku’s management cited data from Comscore CTV Intelligence data. The data for May 2024 showed that 47% of time spent on a CTV device was spent on a Roku device. That’s three times larger than the second-place CTV brand, Amazon.

Just how much time are people spending on Roku’s platform? In Q2 alone, the nearly 84 million households with Roku devices streamed over 30 billion hours of video content. That was up 20% year over year, far higher than its user growth, showing just how much more people are streaming video now.

This is great news from a business perspective. Roku generates a large portion of its revenue from advertising. More people are using its devices and spending more time streaming, which leads to a higher number of advertising opportunities.

Roku’s revenue per user should logically go up as users spend more time streaming on the company’s devices. But this isn’t happening right now. Its average revenue per user over the past year is $40.68 compared with an average of $40.67 per user at this time last year. One would have expected it to grow at least 20% — in line with the growth in hours users spent on the platform.

One problem is that international markets are a large and growing component of Roku’s revenue, and international markets have lower monetization rates. However, that’s not a long-term concern. Over time, higher competition from advertisers in those markets could improve how much the company is paid per ad.

The other problem is with monetization. Roku says its monetization rate mostly grew faster than the overall market. But advertising spend in the media and entertainment categories dropped in Q2.

While concerning at first glance, this might not be too big of a deal either. Consider that media and entertainment brands have spent heavily in recent years to build their streaming platforms. Much of that advertising spend went to Roku since it’s the largest player in the space. Now that streaming platforms are focused on better profits, they’ve pulled back on spending, which hurts Roku.

However, if the rest of Roku’s advertising business is growing faster than the overall market, that would suggest it’s still taking advertising market share.

Is Roku stock a good investment?

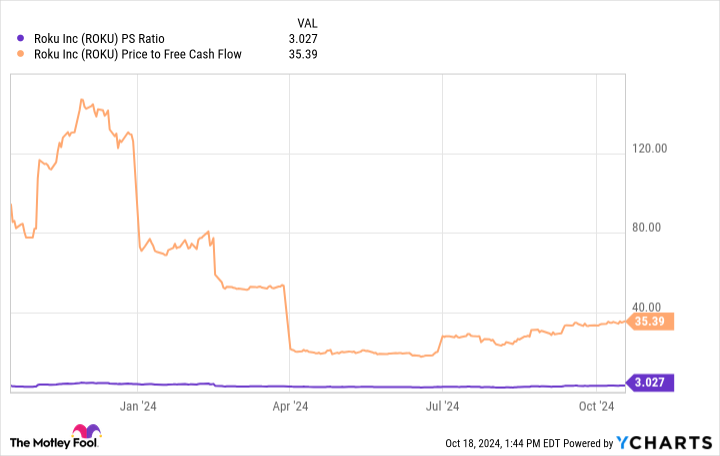

Trading at about 3 times sales and 35 times its free cash flow, Roku stock is reasonably priced if it can grow long term.

ROKU PS Ratio data by YCharts. PS Ratio = price-to-sales ratio.

Regarding competition, Roku has almost half the market — that doesn’t just happen. The company evidently made smart moves to outcompete up until now, and I’ll give it the benefit of the doubt going forward. Third-party research says the space will grow by leaps and bounds. If it holds on to a large percentage of the market, Roku will be a big beneficiary of the industry tailwind.

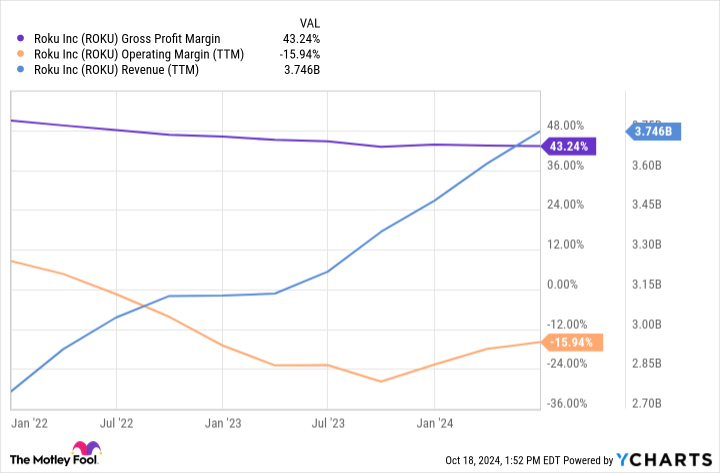

One recurring issue for Roku has been operating leverage with scale — as it has grown, profitability hasn’t improved. Over the last three years, both its gross profit margin and operating profit margin have gone down, even though revenue is way up.

ROKU Gross Profit Margin data by YCharts. TTM = trailing 12 months.

This chart isn’t what investors want to see. But other than this, Roku is aptly positioned in a growing market, and its valuation is reasonable. It needs its profitability to improve, and investors will need to watch that. In the meantime, the consolation is that it’s profitable from a free-cash-flow perspective.

I believe that if Roku’s profit margins improve, it’s set up to be a great investment.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jon Quast has positions in Roku. The Motley Fool has positions in and recommends Amazon and Roku. The Motley Fool has a disclosure policy.